Tax Reform Bill Update

The tax reform bill has passed both houses of Congress and now awaits the President’s signature to become law. The bill includes some sweeping changes along with other, less significant changes, to the existing tax law. Please see our update below including pertinent information and connect with your Edelstein advisor if you have any questions.

Individuals

Standard deduction and itemized deductions:

The amount of the standard deduction is temporarily increased to $24,000 for married individuals filing a joint return, $18,000 for head-of-household filers, and $12,000 for all other individuals.

The suspension of the overall limitation on itemized deductions is effective for taxable years beginning after December 31, 2017 and before January 1, 2026.

All miscellaneous itemized deductions that are subject to the two-percent floor under present law have been repealed.

The threshold for deducting medical expenses shall be 7.5-percent for all taxpayers. This threshold applies for purposes of the AMT in addition to the regular tax. The provision is effective for taxable years beginning after December 31, 2016 and before January 1, 2026.

Personal Exemptions:

The deduction for personal exemptions has been suspended.

Mortgage interest:

For taxable years beginning after December 31, 2017, and beginning before January 1, 2026, a taxpayer may treat no more than $750,000 as acquisition indebtedness ($375,000 in the case of married taxpayers filing separately). In the case of acquisition indebtedness incurred before December 15, 2017 this limitation is $1,000,000 ($500,000 in the case of married taxpayers filing separately. For taxable years beginning after December 31, 2017, a taxpayer may not claim a deduction for interest on home equity indebtedness.

Note: Taxpayers who have entered into a binding written contract before December 15, 2017 to close on the purchase of a principal residence before January 1, 2018, and who purchase such residence before April 1, 2018, shall be treated as having incurred acquisition indebtedness prior to December 15, 2017 under this provision.

State and local taxes:

Taxpayer’s nonbusiness State and local tax deductions, including property taxes, are limited to $10,000 ($5,000 for married taxpayer filing a separate return). Taxpayers can still deduct sales taxes as an alternative to state and local taxes.

Alimony:

The deductibility of alimony and separate maintenance payments by the payer as well as the inclusion into income by the recipient has been suspended. The conference agreement is effective for any divorce or separation instrument executed after December 31, 2018.

Alternative Minimum Tax:

For taxable years beginning after December 31, 2017, and beginning before January 1, 2026, the AMT exemption amount is increased to $109,400 for married taxpayers filing a joint return (half this amount for married taxpayers filing a separate return), and $70,300 for all other taxpayers (other than estates and trusts). The phase-out thresholds are increased to $1,000,000 for married taxpayers filing a joint return, and $500,000 for all other taxpayers (other than estates and trusts). These amounts are indexed for inflation.

New temporary law on various individual tax credits:

Child tax credit increases to $2,000 per qualifying child and up to $500 nonrefundable credit for qualifying dependents other than qualifying children. There are no changes to the definition of a dependent. Of the $2,000 child tax credit, the refundable portion may not exceed $1,400 per qualifying child. In order to qualify for the credit, the child must have a Social Security number issued before the due date for the taxable year. This requirement is not held for the $500 non-child dependent credit. The qualifying child must be under age 17 during the taxable year. The Adjusted Gross Income phase-out for this credit begins at $400,000 for married individuals filing joint tax returns or $200,000 for all other filers. The phase-out rates are not indexed for inflation.

Education savings underwent changes. Qualified education plans, known as 529 plans, are now limited to $10,000 on the expenses paid per year for a public, private or religious elementary or secondary school. (A secondary school is typically referred to middle school and high school. It is the school after elementary and before college.) This limit is on a per child basis, not per-account basis. Any excess distribution above this $10,000 limit will be treated as a taxable distribution under the general rules of section 529.

Section 529 plans can be rolled into qualified ABLE programs established to meet qualified disability expenses. Restrictions apply. The beneficiary of the ABLE account must also be the beneficiary of the 529 plan.

Estate Tax:

The estate tax was not repealed, but rather doubled for estate and gift tax exemptions for estates of decedents dying and gifts made after December 31, 2017, and before January 1, 2026. The generation-skipping transfer (GST) tax is also doubled.

IRAs:

A contribution to a traditional IRA and converting it to a Roth IRA is still allowed. However, unwinding the conversion back to a traditional IRA is no longer allowed.

Maximum retirement contribution limits for 2018 were set by the IRS in October 2017. The maximum contribution for plans including 401(k), 403(b), and most 457 plans increased from $18,000 to $18,500. The catch-up amount for those over age 50 is still $6,000. Traditional IRA and Roth IRA contribution limits are set at $5,500 (no change). The income phase-out range for being able to contribute directly to a Roth IRA is $120,000-$135,000 for single and head of household taxpayers. Married filing joint tax return filers have a phase-out range of $189,000 to $199,000.

Businesses

Bonus Depreciation:

The 50-percent allowance is increased to 100 percent for property placed in service after September 27, 2017, and before January 1, 2023 (January 1, 2024, for longer production period property and certain aircraft). The 100-percent allowance is phased down by 20 percent per calendar year for property placed in service, and specified plants planted or grafted, in taxable years beginning after 2022 (after 2023 for longer production period property and certain aircraft).

It also removes the requirement that the original use of qualified property must commence with the taxpayer, thus, the provision applies used and new purchases.

179 Expensing:

Taxpayers may expense under section 179 to $1,000,000 and increases the phase-out threshold amount to $2,500,000.

DPAD:

Under pre-Tax Cuts and Jobs Act law, the domestic production activities deduction (“DPAD”), which was allowed for certain qualifying U.S.-based activities, was equal to 9% of the lesser of the taxpayer’s qualified production activities income or the taxpayer’s taxable income (determined without regard to the DPAD) for the tax year.

New Law: The Tax Cuts and Jobs Act repeals the DPAD. (Code Sec. 199 repealed by 2017 Tax Cuts and Jobs Act §13305(a))

Effective: Tax years beginning after Dec. 31, 2017. (2017 Tax Cuts and Jobs Act §13305(c))

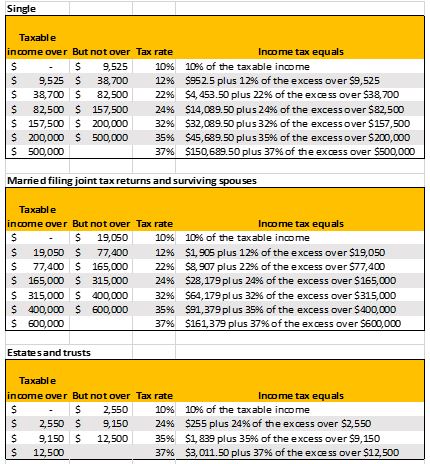

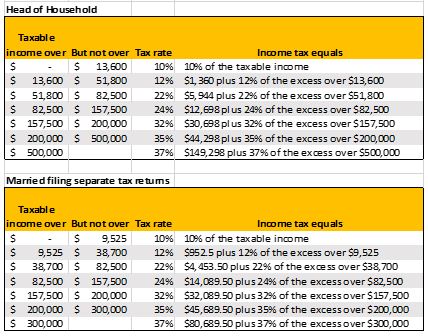

New tax rates

Posted In: Alerts & Advisories, News